The Importance of Insurance Liability Car

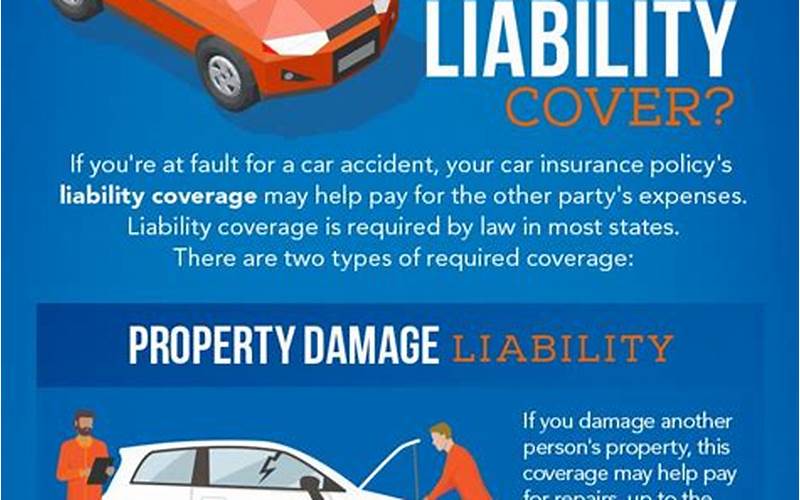

You can never predict when an accident might happen while you’re driving your car. Even if you’re a cautious driver, you can’t control the actions of other drivers on the road. That’s where insurance liability car comes in. It’s a type of auto insurance that provides coverage for damages or injuries that you may cause to others while driving your car. In other words, it protects you from any legal liabilities that may arise from an accident.

Without insurance liability car, you could be held responsible for paying for damages or medical bills out of pocket. That could be a financial burden that could take years to pay off. However, with insurance liability car, you can have peace of mind knowing that you’re protected against any unforeseen circumstances on the road.

What Exactly is Insurance Liability Car?

Insurance liability car is a type of auto insurance that covers any damages or injuries that you may cause to others while driving your car. This means that if you’re at fault in an accident, your insurance company will pay for the damages or medical bills of the other party. It’s important to note that insurance liability car only covers damages or injuries that you’re legally responsible for. If the other party is at fault, their insurance will cover the damages.

There are two types of insurance liability car coverage: bodily injury liability and property damage liability. Bodily injury liability covers any medical expenses or lost wages that the other party may incur as a result of the accident. Property damage liability covers any damages to the other party’s property, such as their car or fence. It’s important to have both types of coverage to ensure that you’re fully protected in the event of an accident.

How Much Insurance Liability Car Should You Have?

The amount of insurance liability car coverage you should have depends on your individual circumstances. However, most states require a minimum amount of coverage that you must have to legally drive your car. The minimum amount varies from state to state, but it usually ranges from $20,000 to $50,000 for bodily injury liability per person and $50,000 to $100,000 for bodily injury liability per accident. Property damage liability coverage usually ranges from $10,000 to $25,000.

While the minimum coverage may be enough to legally drive your car, it may not be enough to fully protect you in the event of an accident. It’s recommended that you have at least $100,000 of bodily injury liability coverage per person and $300,000 per accident, as well as $100,000 of property damage liability coverage. Of course, the more coverage you have, the better protected you’ll be in the event of an accident.

What Factors Affect Your Insurance Liability Car Premium?

The cost of your insurance liability car premium depends on several factors, including your age, driving record, location, and the type of car you drive. Younger drivers and those with a poor driving record may have higher premiums than older drivers with a clean record. Additionally, those who live in high-risk areas or who drive expensive cars may also have higher premiums.

Another factor that affects your insurance liability car premium is the amount of coverage you have. The more coverage you have, the higher your premium will be. However, it’s important to have enough coverage to fully protect yourself in the event of an accident.

How to Save Money on Insurance Liability Car

While insurance liability car is necessary to protect yourself and your car, it can also be expensive. Fortunately, there are several ways you can save money on your premium. One way is to shop around and compare quotes from different insurance companies. You may find that some companies offer lower premiums for the same amount of coverage.

Another way to save money on insurance liability car is to bundle your coverage with other types of insurance, such as homeowners or renters insurance. Many insurance companies offer discounts for bundling multiple policies.

You can also save money on your premium by raising your deductible. The deductible is the amount you pay out of pocket before your insurance kicks in. By raising your deductible, you’ll lower your premium. However, make sure that you can afford to pay the higher deductible if you’re ever in an accident.

What Happens if You Don’t Have Insurance Liability Car?

Driving without insurance liability car is not only illegal, but it can also be financially devastating if you’re ever in an accident. If you’re caught driving without insurance, you could face fines, license suspension, and even jail time in some states. Additionally, if you’re at fault in an accident and don’t have insurance, you’ll be responsible for paying for any damages or medical bills out of pocket. This could amount to thousands of dollars or more, depending on the severity of the accident.

Not having insurance liability car is simply not worth the risk. It’s important to have coverage to fully protect yourself and your car in the event of an accident.

FAQs About Insurance Liability Car

1. Does insurance liability car cover damages to my own car?

No, insurance liability car only covers damages or injuries that you may cause to others while driving your car. If you want coverage for damages to your own car, you’ll need to purchase additional coverage, such as collision or comprehensive insurance.

2. Do I need insurance liability car if I don’t own a car?

If you don’t own a car, you may not need insurance liability car. However, if you frequently rent or borrow cars, you may want to consider purchasing a non-owner car insurance policy, which provides liability coverage when you’re driving a car that you don’t own.

3. Is insurance liability car required by law?

Yes, insurance liability car is required by law in most states. The minimum amount of coverage varies from state to state, but you must have at least the minimum amount to legally drive your car.

4. Will my insurance liability car cover me if I’m driving someone else’s car?

Typically, insurance liability car covers the driver, not the car. This means that if you’re driving someone else’s car and cause an accident, your insurance will cover the damages or injuries to the other party. However, if the car owner has insurance, their insurance may also provide coverage in the event of an accident.

5. Can I get insurance liability car if I have a poor driving record?

Yes, you can still get insurance liability car if you have a poor driving record. However, your premium may be higher than someone with a clean record. It’s important to shop around and compare quotes from different insurance companies to find the best rate.

6. Can I add additional drivers to my insurance liability car policy?

Yes, you can usually add additional drivers to your insurance liability car policy. However, the cost of your premium may increase if you add drivers with a poor driving record or who are under the age of 25.

7. How often should I review my insurance liability car coverage?

It’s a good idea to review your insurance liability car coverage at least once a year to ensure that you have enough coverage. If you’ve recently purchased a new car, moved to a new state, or had any other major life changes, you should also review your coverage to make sure you’re fully protected.

Conclusion

Insurance liability car is an essential type of auto insurance that provides coverage for damages or injuries that you may cause to others while driving your car. Without insurance liability car, you could be held responsible for paying for damages or medical bills out of pocket, which could be a financial burden. It’s important to have enough coverage to fully protect yourself in the event of an accident. While insurance liability car can be expensive, there are several ways you can save money on your premium, such as shopping around, bundling your coverage, and raising your deductible. Don’t risk driving without insurance liability car – it’s simply not worth it.

Remember to review your insurance liability car coverage at least once a year, and make sure you have enough coverage to fully protect yourself and your car in the event of an accident. Hopefully, this article has helped you better understand insurance liability car and why it’s so important to have. Stay safe on the road!